To qualify for a mortgage, many financial aspects are considered; buyer income, debt ratio, property value, and credit. Having an understanding of how each of these categories work, intertwines with one another, and how that interaction ultimately affects the success of the transaction, will allow you to be better prepared when seeking financing.

Important aspects of mortgage approval

Income:

Banks will want to see consistent income and a history of consistent work to prove regular employment. Income is a crucial factor, it will determine whether or not approval from the bank is likely. If an individual does not earn enough income to pay back a loan then no matter what their credit score, debt, or appraisal might be, the bank will not approval the loan.

Debt:

Next is debt. Most banks will use an equation that subtracts outstanding debt from your income to help determine the rate and loan quantity. If the buyers debt; credit cards, student loans, car loans, and/or the pending mortgage loan, are higher than the income affords, the bank will not give approval. Get those credit cards paid off before applying for a mortgage, if they are very high the debt may damage the mortgage amount you can qualify for. Banks usually have a debt-threshold for mortgage approval, if you’re above this threshold they will deny you.

Property value:

How much does the home appraise for? Does the bank agree that it’s worth that amount? Banks want to make sure the home is being bought for a reasonable price, that they (the buyer) are not being overcharged. Banks will consider property value before approving the mortgage.

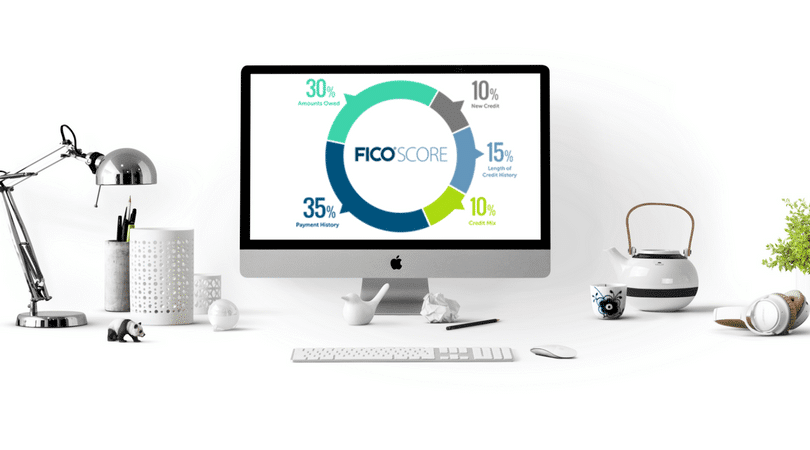

Credit:

Lastly, banks will look at your (and any co-signer’s) credit. Credit reports and scores give lenders a look at payment patterns and history of past financial commitments, if the buyer has an extended history of paying on time they are more likely to be considered for the mortgage they’re seeking. Again, most lenders have a threshold for loan approval, they will not sign off on a loan if the applicants score is below this threshold.

Changes in our national economy can drastically changed the outlook lenders have on loan approval. In the past, banks have suffered huge losses with so many properties going into foreclosure and short sale that they have become increasingly more dependent on an individual’s credit history in determining their ability to make timely payments. Credit is the only way a bank can see an individual’s track record of payments over the last 7-20 years. This supersedes a person’s income, debt ratio, and property value when determining whether or not they qualify and even the interest rate at which to charge the loan.

If you plan on purchasing a home obtain a copy of your credit scores and reports, this way you’ll be ‘in-the-know’ and possibly able to fix any errors or negative information. This can give you more opportunity to have a successful purchase at the best rates possible.