Business owners using personal assets & credit

It’s common for principals to rely upon their personal assets and credit to fund business operations while revenue is low or when first starting out. Business owners often make the mistake of relying too much on their personal finances and mixing their business and personal credit/assets.

What should happen is as the business grows and brings in profits, owners should work to establish and build business credit, so they will have more options when it comes time to secure affordable business loans and lines of credit. Once you establish business credit, you will have more funding options that do not require a personal guarantee. Despite the information growth, many small businesses still do not see business credit as a priority.

The prevalence of this issue is suggested in the 2016 Small Business Credit Survey that was released in April 2017.

The purpose of this study was to provide insight on the access to credit and demand for credit being made by small to mid-size businesses throughout the country.

This report was generated and presented through a collaboration of 12 Federal Reserve Banks, 10,303 employer firms from across the nation participated. Out of participating the firm’s 70% were small businesses with an annual revenue of less than $1 million and the remaining 30% being mid-size companies with an annual revenue of greater than $1 million.

Out of the 10,303 firms that participated:

- 65% are a low credit risk, 27% a medium risk, and only 8% high risk.

- 65% male owned, 20% female owned, and 15% equal ownership.

- 61% of all the firms reported being faced with financial issues over the past 12 months & 44% of all firms reported their major financial challenge was related to a lack of credit availability to expand.

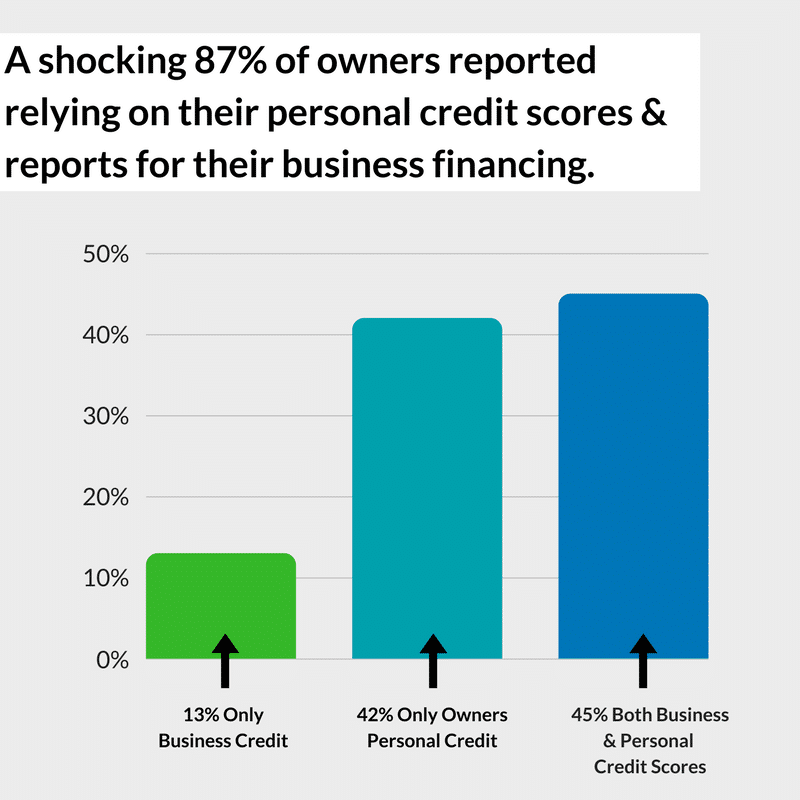

Business owners reported often relying on their personal credit & assets.

76% of all the firms said they resolved financial challenges by using their personal assets

Source: 2016 Small Business Credit Survey; Federal Reserve Banks of Atlanta, Boston, Chicago, Cleveland, Dallas, Kansas City, Minneapolis, New York, Philadelphia, Richmond, San Francisco, and St. Louis.

When it came to obtaining business financing, principals reported using their personal credit/finances to secure business loans/line of credit. As might be expected, the smaller the firm was, the more they relied upon personal assets rather than outside financing.

Reasons why business owners choose to rely on their personal credit but neglect their business credit

- Many still do not understand that their business credit is reported separately from their personal credit.

- There is a lack of information made available to business owners, they may think that business credit is built the same as personal credit. Some owners do not realize the importance of company credit until they apply for a loan or line of credit through a vendor and get denied or offered a loan with exorbitant fees.

- Nearsightedness – Building and establishing business credit takes time and effort, it’s likely the last thing on your mind. It may be easier for a business in a bind to take out a loan with a personal guarantee.

- Some firms, who do have business credit, have trouble getting approved by just their business credit factors due to their financials/receivables or the amount of time the firm has been in business.

When mixing business and personal finances

There is nothing wrong with offering a personal guarantee, but having strong business credit in addition to personal, can help secure affordable rates. Be responsible when offering a personal guarantee, if you default on the loan and damage is done to personal credit due to business challenges, it can lead to a denial of personal financing like for a mortgage or car loan.

There are different types of financing that one might sign personally for as a principal of a company. Some will have a great impact on personal credit scores and personal loan approvals while others will not show on credit unless a default on the payments occur.

For example:

- Some business credit cards show up on personal credit. If a business owner carries very high balances for the business it could drop scores 20, 60, or even 100 points depending on the rest of their credit. This might price out a mortgage at a cost of hundreds of thousands of dollars more over the life of the mortgage.

- When a business has excellent credit and the owner has excellent personal credit. Depending on the company’s financials, they may get approved for a $100,000 business line of credit at a very low rate. The principal can use this line at their discretion based on need and the balance (although they signed personally) will not show on personal credit unless he/she defaults.

There are also loans, lines, and more for businesses that are not guaranteed by the principal. There is usually a cost for such loans. Fees or interest may be much higher, and the time involved in paying the lender back may be much shorter. These can be excellent options and will eliminate personal liability, but must be investigated, weighed, and compared.

What you don’t know can hurt you!

Business credit and business lending is highly unregulated. Because business lenders, creditors, vendors, and credit bureaus have no regulation forcing them to divulge how your business credit is used or viewed, there is little information and education explaining this to those impacted by it.

There is no motivation for a bank to inform you they reviewed your credit and rejected, denied, or charged you higher pricing for line/loan based on what they viewed. Most commercial lender reps don’t even realize both business and personal credit is analyzed before loan approval and pricing is offered. Not only can a bank review your business credit but anyone (even potential and current partners and accounts) can pull your business credit and make decisions that could cost your firm millions without you ever knowing.

So what should a business do to make sure they are presenting the best possible first/longstanding impression?

- Review all the major business bureaus (mention them with links) since they are the most common that can be reviewed.

- Find out from your factoring company, lenders, vendors, or anyone extending credit to you, which credit bureaus they use? There are many small bureaus as well as the major three.

- If the bureau used is different than the major bureaus find out how to get a copy of your business credit from them.

If you need assistance and would like us to help you understand the reports we would be happy to give you a free credit review and help you gain insight into what would help your business make the best impression and gain the most opportunity that great business credit can offer.